While the formulas used to calculate FICO credit scores are proprietary, over time and with experience our team has gained key insights about this mystical creature.

While no one really knows what truly makes up the score - or why and when it moves up or down - there are some basic assumptions to help improve your credit score and get you on the right track when it comes time to apply for a mortgage loan.

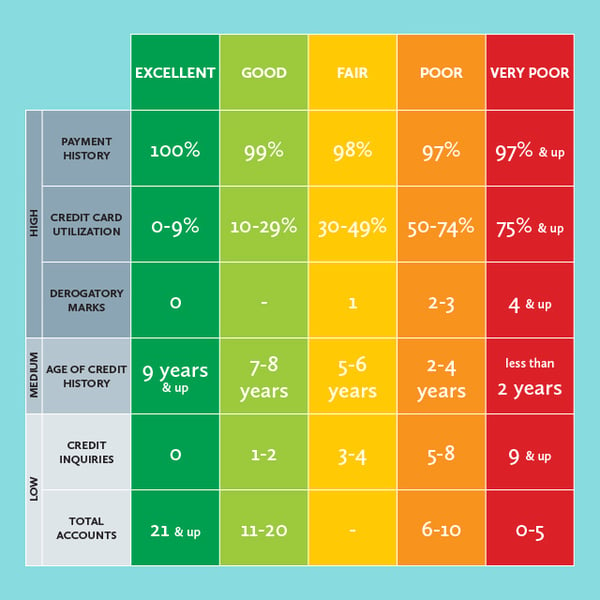

Factors that Impact Your Credit Score

According to myFICO, your past long-term payment behavior is used to predict future behavior - making payment history one of the most important components of your overall credit score, determining 35% of your FICO® Score!

Being proactive about your credit score is the best way to prepare for the future - especially if you're planning on buying a new home.

Getting a sense of what your monthly mortgage payment would be based on the sales prices of homes in your area is a great way to narrow down your focus, this mortgage calculator breaks down the details of your payment, too.

PRO TIP: Understanding the impact of your credit score on your mortgage loan application can help you identify key areas to focus on.

Top 2 Credit Score Tips Homebuyers Should Know

Tip #1

Always, always, always make sure your minimum payment is always made on ALL debt obligations. A single late payment could drop your credit score 100 points or more and does not recover quickly. A payment is considered late when it reaches 30 days past due.

Tip #2

Keep all credit card balances at 30% or less of their max limit. If you have a $1,000 limit on a card, be sure not to charge more than $300. What we've seen is that when credit cards are used above 30% of the max limit, scores begin to decrease. If you're currently over 30%, no worries - as you bring the balance down you'll see your score rise!

Click here to reach out to me for more tips, help with mortgage questions, or to apply online - I'm happy to help! - Jamie

Check out our latest guide, Mortgage Loan Processing Do's & Don'ts:

Featured Expert

Jamie Cooley is a Sr Loan Originator with Fairway Independent Mortgage Corporation and has been recognized as a Top 1% Mortgage Originator in America the last 5 years. Jamie is an Omega Builders preferred lender and works closely with our home buyers to ensure a smooth closing from start to finish.

NMLS# 1044127

This article is provided for informational purposes only. Omega does not warrant or guarantee the accuracy of the information provided and makes no representations associated with the use of this information as it is not intended to constitute financial, legal, tax, or mortgage lending advice. Omega Builders encourages you to seek the advice of professionals in making any determination regarding, financial, legal, tax, or mortgage decisions as only an informed professional can appropriately advise you based upon the circumstances unique to your situation.